The 7 Financial Choices You’ll Regret 5 Years From Now

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

Published May 19, 2025

Paying off your credit card in full is better because it lowers debt and avoids interest. Making payments on time also boosts your credit score, so carrying a balance isn’t needed.

Figuring out whether to pay off your credit card in full or carry a balance can be confusing, especially with the conflicting advice out there. Some say carrying a balance helps your credit score, while others insist paying in full is best. The truth is that how you manage your credit card affects your credit score, interest rates, and future loan approvals.

In this guide, we’ll clear up the confusion, explain why paying in full matters, and share the best strategies for managing credit card debt.

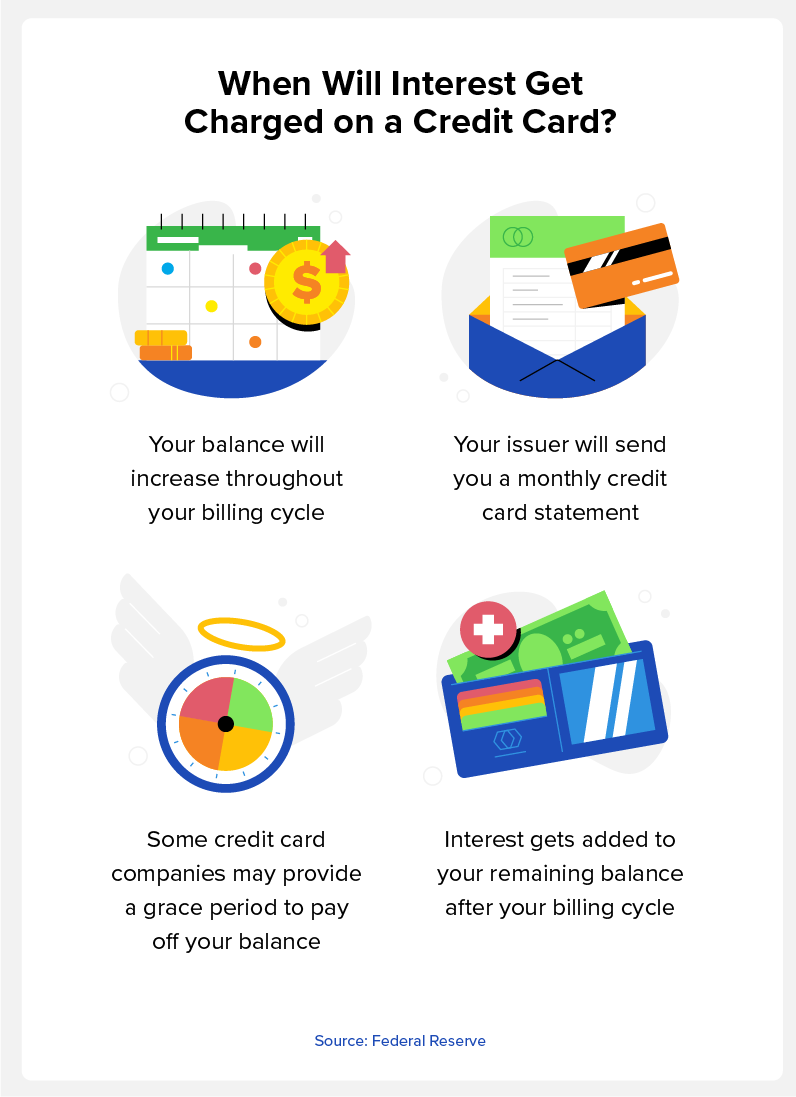

Your credit card balance is the total amount you owe to your card issuer at any given time. It changes as you make purchases, incur fees, or pay down debt. Understanding what makes up your balance can help you manage your credit wisely and avoid unnecessary interest charges. It includes:

Your balance changes as you make new purchases, pay down debt, or incur fees and interest. Paying off your balance in full each month can help you avoid interest charges and maintain a healthy credit score.

Paying off your credit card in full each month eliminates debt and reduces financial stress. It also saves you from interest charges and improves your credit utilization ratio, which is crucial for maintaining a strong credit score.

A low credit utilization ratio and on-time payments make you a more attractive borrower. They increase your chances of qualifying for better credit cards, loans, and lower interest rates. Paying in full also frees up your credit limit, giving you more flexibility for future spending.

Consistently paying off your balance helps build responsible credit habits, demonstrating to lenders that you can manage debt wisely and strengthening your credit profile over time.

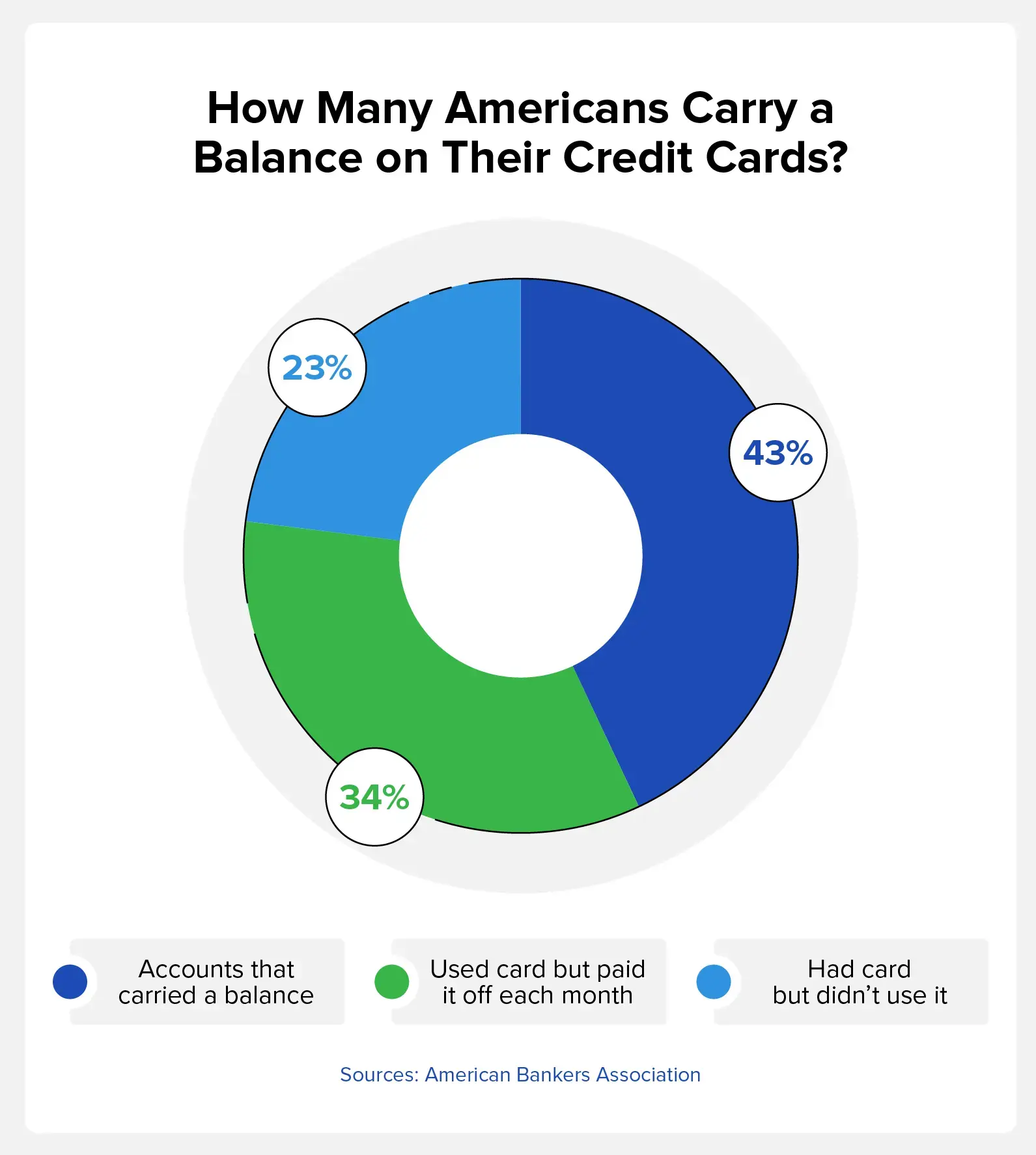

On the other hand, carrying a balance can lead to higher interest rates and harm your credit score, particularly if your balance is close to your credit limit. High credit utilization can negatively impact your score, even if the balance is small.

Credit utilization, or your “amount owed,” is worth 30% of your FICO® credit score, making it the second most important factor next to your payment history. To avoid a low credit score, your credit utilization should be lower than 30% of your total credit limit. Your total credit limit is the sum of all your credit card limits.

For example, if you have three credit cards with maximum limits of $500, $700, and $800, your total credit limit is $2,000. To keep a good credit utilization ratio, your total amount owed should be less than $600. Even if you reach the limit on one card, you can still maintain a healthy score as long as the total balance on all cards remains within your ideal utilization range.

One strategy to help manage credit utilization is the 15/3 method. This involves making a payment on your credit card 15 days before your statement date to lower your balance, then paying the remaining balance in full 3 days before the due date. It ensures your balance is reported low to the credit bureaus, which can help maintain a lower credit utilization ratio and potentially improve your score.

A high credit utilization ratio can signal to lenders that you're struggling with debt, which could negatively affect your credit score. By paying off your balance each month or using methods like the 15/3 approach, you can keep your credit utilization low, improving your chances of maintaining or achieving a good credit score.

Your credit card balance plays a major role in shaping your credit health. Whether you pay it off in full each month or carry a balance, it directly impacts key factors that influence your credit score. Here’s how:

One of the best strategies to ensure you pay your card off in full each month is to set up automatic payments. Many credit card providers also offer this option when you set up your payments. Now, you may be wondering which day of the month is best to pay your bill, depending on your situation.

Here are some strategies and considerations before choosing a date:

Each credit card issuer reports to the major credit bureaus, Experian®, Equifax®, and TransUnion®. Ideally, you want to pay your balance before they report to the bureaus to ensure you have a low credit utilization.

Unfortunately, each card issuer may report on different dates.

By setting up automatic payments before the due date, you can avoid carrying a balance to maximize your chances of ensuring low credit utilization when the issuer reports to the bureaus.

Many people have irregular paydays or fluctuations in their income. If you’re in this scenario, it may be helpful to make multiple payments per month. Similar to paying before the due date, even if you pay in small amounts, your utilization will remain low if you pay the balance before the due date.

A great way to reach your goal of paying off your balance in full each month is to create a budget. You can create different budget categories so you know how much you can allocate to food, bills, and your credit cards. If you currently have credit card debt that you want to pay off and boost your credit score, we have six of the best strategies to make it happen.

The debt snowball method is one of the most popular methods for paying down credit card debt. The idea behind this method is to build momentum with quick wins, which can motivate you to continue paying off your credit card debt.

This method involves paying off your credit card with the smallest balance first, then the card with the next smallest balance, and so on, until you pay off the card with the most debt.

Disadvantages: You may pay more in credit card interest over time.

The debt avalanche method is the opposite of the snowball method. Rather than starting with your smallest debt, you start with the largest one.

You could also start with the card that has the highest interest rate and work your way down to the one with the lowest interest rate. The primary benefit of this method is that it helps reduce the total amount you’ll pay by reducing the interest fees.

Disadvantages: Getting your first win can take some time, so you don’t benefit from the momentum and motivation like you would with the snowball method.

Balance transfer cards help pay off your debt by simplifying your payments and lowering your interest rate. These cards work by allowing you to transfer your debts from different credit cards to a single card.

Ideally, the balance transfer card will have a better interest rate. If you struggle with remembering to pay each of your individual cards, having a single payment can help.

Disadvantages: There’s often a fee for transferring your debt, and if you don’t pay it off in the specified time, the interest rate may be higher than your original cards.

A debt consolidation loan is similar to a balance transfer card, but it’s a personal loan. To get a debt consolidation loan, you’ll need to go to a bank and get a loan for the amount you owe on all of your credit cards.

You can then make one monthly payment to the bank to pay off your loan rather than paying off multiple credit cards. You may have a lower interest rate as well.

Many people also use debt consolidation as an alternative to bankruptcy because it helps get their debts under control.

Disadvantages: You need good credit to qualify for a debt consolidation loan.

If you don’t want to take out a debt consolidation loan or use a balance transfer card, increasing your income can help you pay off your debts. You can increase your income by asking for a raise at work or using your skills and resources to pick up a side hustle. There are many ways to make money online, and your extra income may cover your monthly credit card bills.

Disadvantages: You may not be able to get a raise, and side hustle income may be inconsistent.

Sometimes, the best option is to turn to a friend or family member to pay off your debts. Borrowing from someone you know is similar to a debt consolidation loan. The primary benefit is that a friend or family member most likely won’t charge you fees or interest.

Disadvantages: Borrowing from a loved one can harm the relationship if you can’t pay the money back.

The following are some of the most common questions about paying off your credit card balance each month.

The amount of points you get for paying off your credit cards will vary. It primarily depends on your credit utilization. Paying off a larger balance if you’re close to your limit will boost your score more than if your utilization was already low. You can typically expect a three- to 10-point increase.

The best way to pay off a credit card is to pay it off in full each month, and there are different strategies you can use, like creating a budget and a personal spending limit. If you’re unable to pay off the balance in full, the goal should be to keep your credit utilization under 30%.

If possible, you should pay off your credit card’s entire balance each month. By only making minimum payments, you can accrue interest fees, which will cost you more money in the long run.

Paying off your credit card after every purchase isn’t necessary, but it can be beneficial. Paying right away keeps your credit utilization low and prevents debt from piling up. However, most cards offer a grace period, so you'll avoid interest as long as you pay your balance in full by the due date. The key is staying consistent and not carrying a balance.

Paying off your credit card in full each month is a great way to avoid debt and interest fees, and it helps boost your credit score. A good credit history and credit utilization ratio are primary factors in your credit score, but many people don’t know where their credit health stands.

If you want a breakdown of your credit score and credit health, sign up to get your free credit report card from Credit.com today.

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.