The 7 Financial Choices You’ll Regret 5 Years From Now

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

Published May 28, 2025

Your credit score may improve if your collection debt is reported to a new credit scoring model—FICO® Score 9, FICO Score 10, VantageScore® 3.0, or VantageScore 4.0. However, most creditors still report to old scoring models.

If you’ve gotten behind on payments to a creditor or lender, your debt could go to collections after around 120 days of missed payments. Your credit score has likely taken a hit as a result, and you may be asking, “Does paying off collections improve your credit score?”

Find out what it means to have collections debt, how it affects your credit, and how you can raise your score after a hit from collections.

When you default on a payment, the company you owe may sell your debt to a third-party collection agency. When this happens, it means your debt has gone to collections, and debt collectors from the collection agency will try to contact you for payment.

Several kinds of debts can go to collections, including:

The time it takes the original creditor to transfer your debt to collections varies. Some contracts may have a grace period where you can still pay your debt after it’s due. In other cases, creditors may send you to collections the day after your payment is due.

Collections debt shows up as a negative mark on your credit and, as a result, will significantly harm your credit. This is because collections fall under the payment history credit factor, which accounts for 35% of your FICO credit score, making it the biggest impact on your score.

The effect on your credit may depend on what your score was to begin with. For example, a score in the 700s may take a more dramatic hit than a score in the 500s.

It also depends on the type of debt you have in collections. Recent changes to how creditors report medical debt to credit bureaus have significantly improved consumer protections.

Now, medical debts are essentially removed from credit reports that lenders use. This means unpaid medical bills, regardless of the amount, will generally not affect your credit score when applying for loans. Additionally, credit bureaus won’t factor paid medical collection debt into your credit report.

The impact of negative collection marks also decreases with time and eventually falls off your report, generally after seven years, as part of the Fair Credit Reporting Act (FCRA).

Paying off collections can help your credit score if the lender reports to new credit scoring models, including FICO® 9, FICO 10, VantageScore® 3.0, and VantageScore 4.0. These models ignore collections with a balance of zero, so you’ll see a boost in your score if you pay off collection debt.

However, if your lender reports to older scoring models, which most do, you likely won’t see a difference in your score even if you pay the debt. These models don’t lessen a negative mark from collections regardless of whether it’s marked as paid or unpaid.

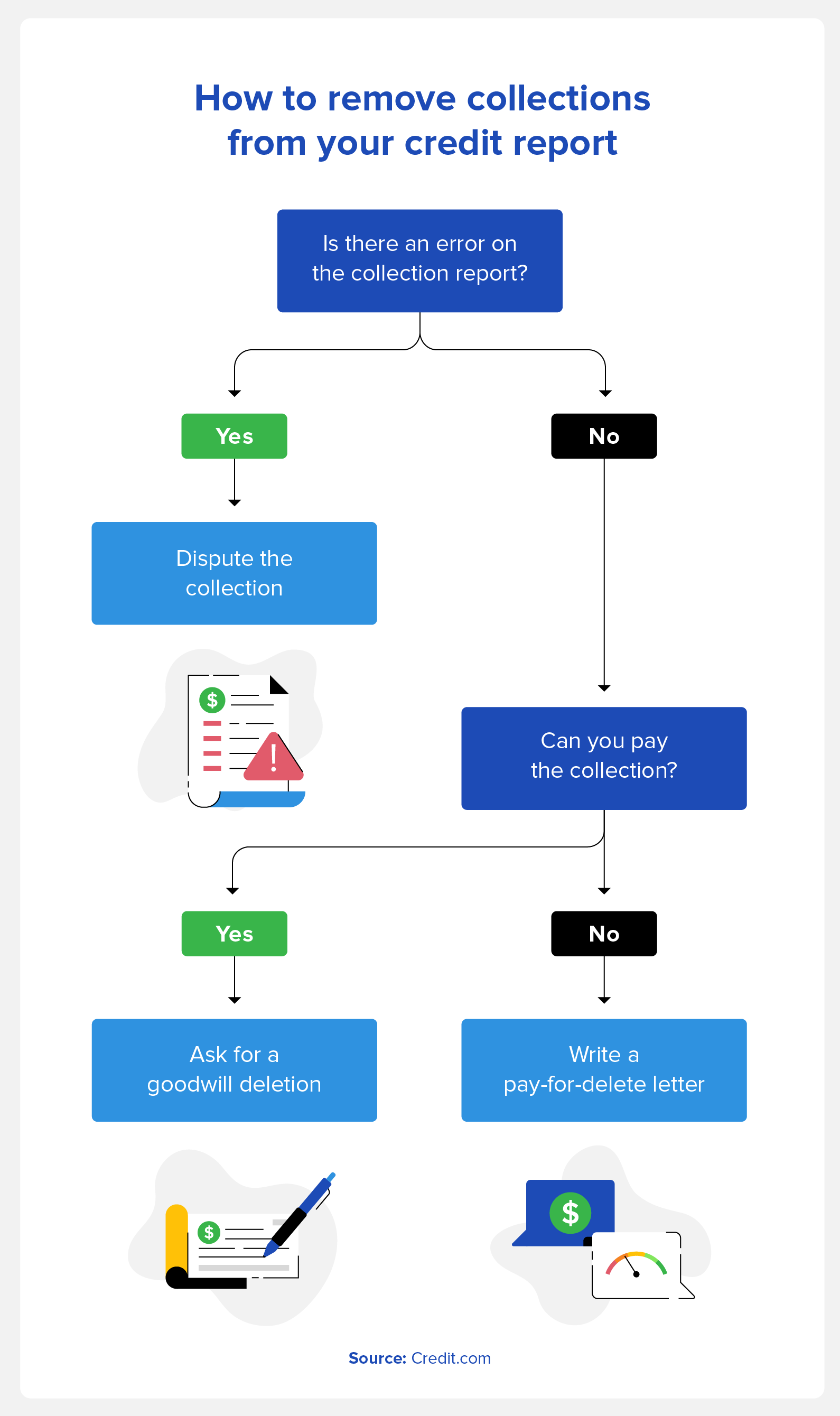

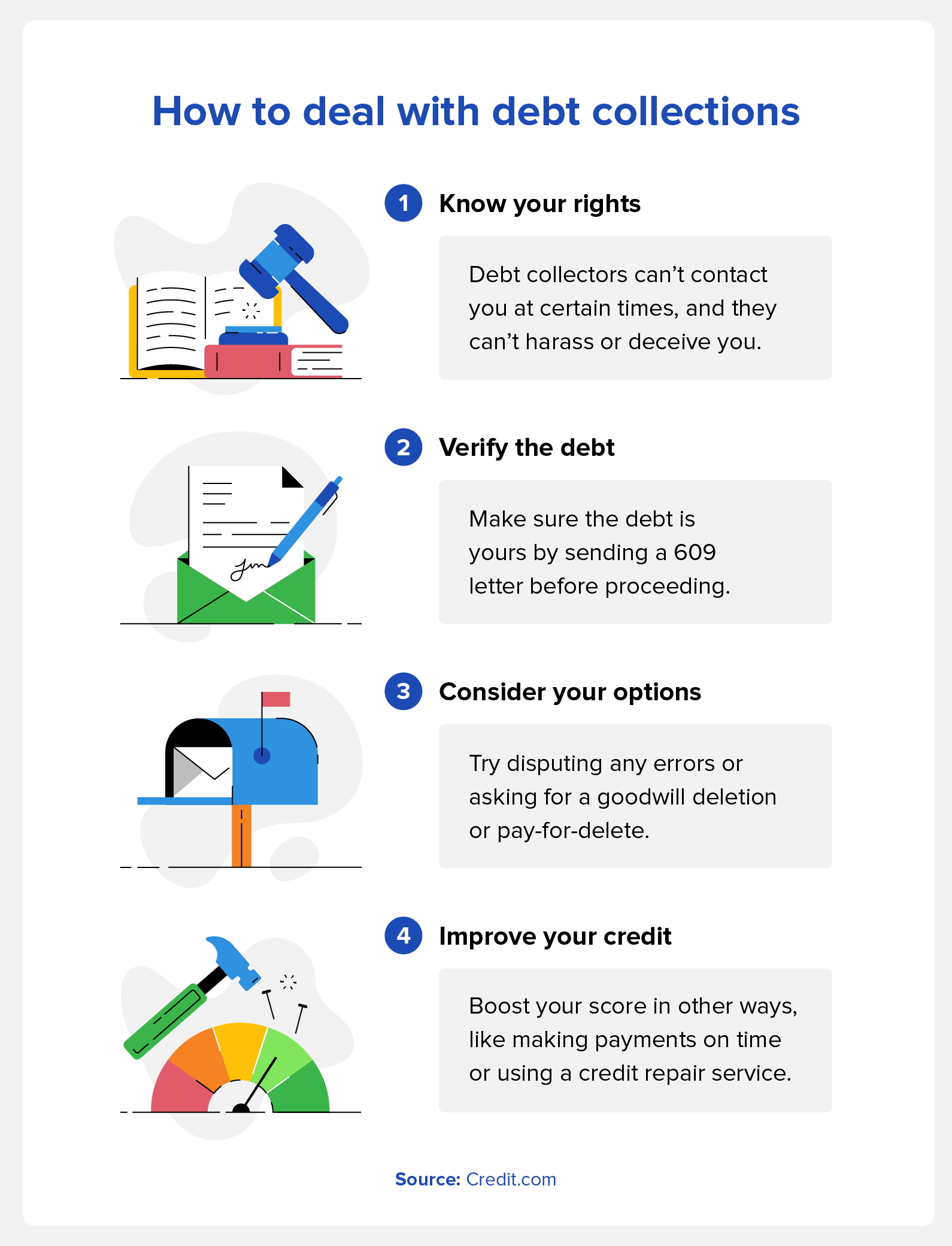

There are a few methods for removing collections debt from your credit report. Keep in mind that results may vary as each individual’s financial situation is different. Here are a few ways you can attempt to get collections removed from your report.

You have the right to dispute any items on your credit report that are inaccurate or outdated. Here are the steps to take to find and challenge errors on your credit report:

Depending on various factors, removing mistakes on your credit report can help raise your credit score. However, disputing errors can be difficult and long.

Consider working with dedicated credit professionals who have experience working with credit bureaus. This is especially beneficial if you have a lot of inaccurate collection accounts or a more complicated situation.

If you have an otherwise positive credit history and a long-standing relationship with the creditor of your collection, you may be able to receive a goodwill deletion.

This process begins with writing a goodwill letter to the original creditor of the collections, which should include:

If successful, the creditor will delete the item you’ve highlighted as a gesture of goodwill.

You may be able to arrange a deal with your collection agency to delete the collection account in exchange for payment. To do this, you can use a pay for delete letter.

Keep in mind that not all agencies accept pay for delete letters, especially banks or larger creditors. Collection agencies tend to sell debts, which means your debt may end up with a new agency where you can try this method again.

To write a pay for delete letter, include the following information in your letter:

Before this step, make sure the debt is verified as yours with a debt verification. Also, document any communication from the collection agency in writing and keep a copy of your letter.

While paying off collections may not always improve your credit score, it can have other financial benefits. Additionally, there are potential consequences for not paying collections. Ultimately, the decision depends on your financial situation and goals.

Here are some reasons to pay your collection debt:

If your debt has already passed the statute of limitations, debt collectors most likely won’t be able to continue asking for repayment or pursue legal action against you.

However, making a payment or a written acknowledgment of the debt could restart that period, during which you could be sued for the debt again. So, if you decide to pay the debt, it’s best to pay it all at once instead of partial payments to avoid restarting the statute of limitations.

If you haven’t found out already, debt collectors can be very persistent. It’s important to know your debt collection rights and how a debt collection agency is legally allowed to handle your accounts and communicate with you.

As outlined by the Fair Debt Collection Practices Act (FDCPA), debt collectors have to follow these guidelines:

If a debt collector has infringed on any of these rights, you can file a report with your state’s Attorney General’s office or the Federal Trade Commission (FTC).

If none of the above methods for removing collections from your credit report worked for you, there are other ways to improve your credit. Here are some ways to start recovering your credit after collections:

It’s a good idea to follow these tips even if your collection debt is reported to a newer credit scoring model, as it may take time to see improvements to your credit score. Looking for more information about how to understand your credit score and monitor improvements?

Get a free credit report card from credit.com.

Have more questions about debt collections? Check out the answers to these common collections questions.

Collections debt stays on your credit report for at least seven years as part of the FCRA, regardless of whether you’ve paid the debt.

The debt doesn’t go away necessarily, but the negative item will eventually drop off your credit report, and you can no longer be sued for the debt after the statute of limitation time period passes.

A collection debt’s impact on your credit score varies, but it could drop your score significantly. The impact depends on your initial score, with higher scores taking a bigger hit than lower scores. Multiple collections on your credit report could drop your score even more.

Your credit score may not increase at all when you pay off collections. However, if your debt is reported using a newer credit scoring model, your score may increase by however many points were impacted by the collections debt.

It would also depend on the time that has passed since getting the negative mark. You’re more likely to see a positive increase from paying off the collection if it was recently incurred than a collection you’ve had for six years since the effects on your credit lessen over time.

If late payments are hurting your credit score, you may need a little extra help understanding how your credit is impacted and what you can do about it.

It's possible, but unlikely, to have a 700 credit score with collections. Newer credit scoring models and recent medical debt rule changes lessen the negative impact, but older models and non-medical collections still significantly lower scores. A strong overall credit history can mitigate the effect, but collections generally reduce scores.

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.