The 7 Financial Choices You’ll Regret 5 Years From Now

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

Published May 19, 2025

Most people know that saving money for the future is important, but it's unclear exactly how much you should save. Some financial experts recommend saving enough to cover six months of expenses, while others urge you to save 15 percent of your income.

Not to mention, the amount of savings you need widely varies by age since those nearing retirement require more savings than young people who have just entered the workforce.

Below, we've investigated Americans' average savings by age, income, and education level to give you a better understanding of how much money you might expect to have saved at each chapter of your life.

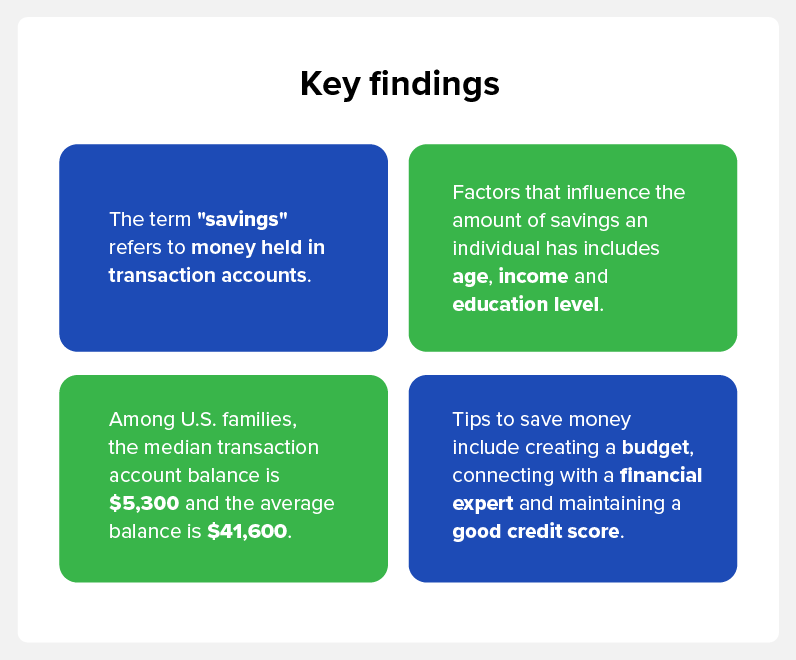

Savings is defined as income that has not yet been spent. Although savings can include investments, in this article, we'll be referring to savings as money held in transaction accounts, such as a checking account, savings account, or money market accounts. Keep in mind that this number doesn't include other assets that may contribute to your net worth.

According to the Federal Reserve Board’s most recent Survey of Consumer Finances, the median transaction accounts balance of all families in 2019 is $5,300 and the average balance is $41,600.

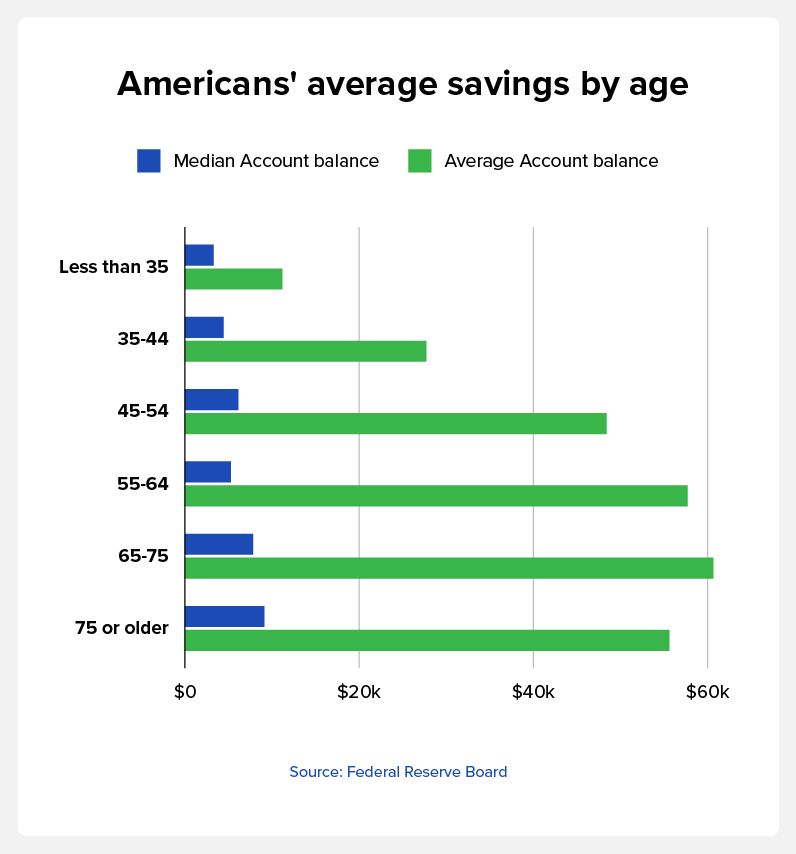

In the chart below, we've organized the Americans' average savings by age. Although there are some exceptions, you can see that the amount of savings tends to rise with age.

| Age |

Median account balance |

Average account balance

|

|---|---|---|

| Under 35 |

$5,400 |

$20,540 |

| 35 to 44 |

$7,500 |

$41,540 |

| 45 to 54 |

$8,700 |

$71,130 |

| 55 to 64 |

$8,000 |

$72,520 |

| 65 to 74 |

$13,400 |

$100,250 |

| 75 or older |

$10,000 |

$82,800 |

While the Federal Reserve doesn’t provide specific data for individuals in their 20s, those under 35 have a median of $5,400 and an average of $20,540 saved in transaction accounts. If you’re in your 20s, you may have less than those numbers, especially if you’ve just graduated from college and entered the workforce.

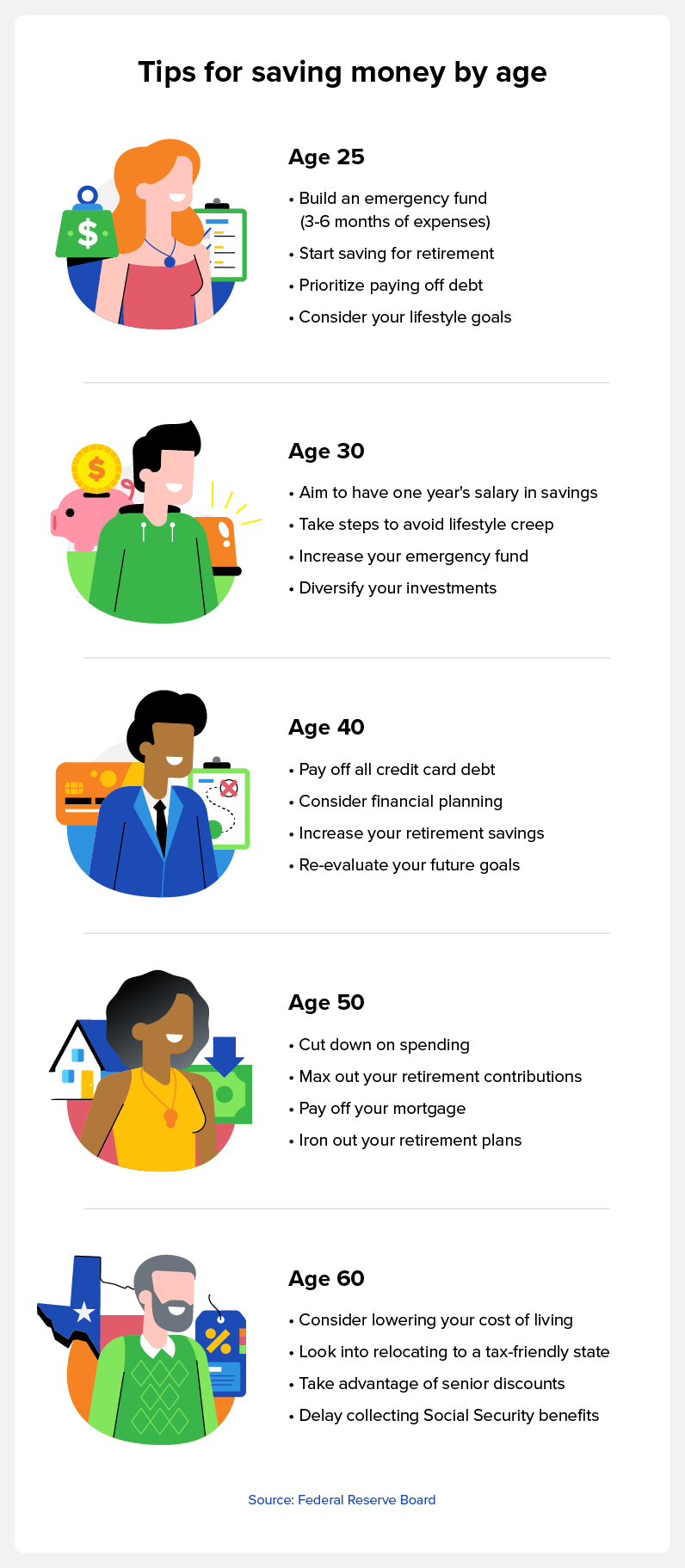

Although it’s not uncommon to have little savings in your 20s, this is the time to develop healthy financial habits that open up opportunities for your future self. Be sure to start contributing to investment accounts if you can to take advantage of the benefits of compound interest, which allows you to earn interest on interest and grow your money over time.

Tips for saving money in your 20s:

As mentioned above, the median account balance among those under 35 is $5,400, and the average balance is $20,540.

By this age, you may have been working for a few years, receiving salary increases that allow you to increase your savings. However, you may also have more expenses than you did previously, especially if you have fallen victim to “lifestyle creep”—a phenomenon that involves increasing your spending as your income increases.

Tips for saving money in your 30s:

Individuals ages 35 to 44 have a median of $7,500 and an average of $41,540 in transaction accounts.

For most Americans, your 40s are when you reach peak earning potential. At the same time, however, expenses may start to rise, especially if you’re making payments on a home or supporting a family. Saving money during this period is crucial if you wish to retire on time.

Tips for saving money in your 40s:

Americans ages 45 to 54 have an average of $71,130 and a median of $8,700 in savings.

At age 50, you may begin to feel more financially comfortable. With retirement approaching in the next decade or so, now is the time to ramp up savings and pay off all debt. Consider maxing out your retirement contributions every year to boost your savings.

Tips for saving money in your 50s:

Individuals ages 55 to 64 have an average of $8,000 and a median of $72,520 in savings. Meanwhile, those between the ages of 65 and 74 have an average of $100,250 and a median of $13,400 saved. Finally, those ages 75 or older have an average of $82,800 and a median of $10,000 in transaction accounts.

By age 60, you may be nearing retirement. During retirement, managing your finances may look different as your focus shifts from growing your finances to saving them. Although you definitely want to enjoy your retirement, it’s also important to stick to a budget to make sure your funds last.

Tips for saving money in your 60s:

In addition to saving money in transactional accounts, it’s also important to save specifically for retirement. The following chart outlines how much the average American has in retirement savings organized by age. As you can see, retirement savings grow with age and then seem to plateau around age 55 to 64. This is likely due to the fact that the average retirement age among retirees is 62, according to Gallup research.

By looking at this chart, you can get a sense of if you’re on track with your retirement goals.

| Age |

Median account balance |

Average account balance

|

|---|---|---|

| Under 35 |

$18,880 |

$49,130 |

| 35 to 44 |

$45,000 |

$141,520 |

| 45 to 54 |

$115,000 |

$313,220 |

| 55 to 64 |

$185,000 |

$537,560 |

| 65 to 74 |

$200,000 |

$609,230 |

| 75 or older |

$130,000 |

$462,410 |

In addition to age, Americans’ average savings vary due to other factors, such as income. As seen in the following data, those with higher income levels are able to save more. The most significant difference in savings is between individuals who earn between $80,000 and $89,999 and those who make between $90,000 and $110,000.

| Income |

Median account balance |

Average account balance

|

|---|---|---|

| Less than $20,000 |

$900 |

$7,860 |

| $20,000 to $39,999 |

$2,550 |

$16,410 |

| $40,000 to $59,999 |

$7,400 |

$25,200 |

| $60,000 to $79,999 |

$15,760 |

$44,070 |

| $80,000 to $89,999 |

$33,800 |

$76,940 |

| $90,000 to $100,000 |

$111,600 |

$353,030 |

There is also a correlation between average savings and education level. The chart below shows that the largest difference in savings is between those who completed some college and those with a college degree. This is likely due to the fact that a college degree is required for many high-paying careers.

| Education level |

Median account balance |

Average account balance

|

|---|---|---|

| No highschool diploma |

$900 |

$9,130 |

| High school diploma |

$3,030 |

$23,380 |

| Some college |

$5,200 |

$33,410 |

| College degree |

$23,370 |

$116,010 |

The Fed’s Survey of Consumer Finances doesn't provide the average retirement savings for married couples by age, but we can see how couples differ from individuals. A couple with children has an average of four times more money in their transaction accounts than a single individual. Couples without children have an average of five times more money in their transactional accounts than single individuals without children.

| Family Structure |

Median account balance |

Average account balance

|

|---|---|---|

| Single with children |

$2,400 |

$16,800 |

| Single, no children |

$4,000 |

$19,320 |

| Couple with children |

$12,500 |

$73,890 |

| Couple, no children |

$16,000 |

$103,140 |

Saving money ensures that you're prepared for the future. Not only does it give you peace of mind, saving money allows you to have more choices regarding your lifestyle. Whether you're saving to make a big purchase or wish to travel the world, your savings can help you reach your goals.

Not to mention, it's important to save for an emergency. That way, you have a sense of security in the event an unexpected expense occurs, such as a home repair, job loss, or injury.

Now that you know the importance of saving your money, we've outlined some tips to help you get started below:

Saving money is important for fostering financial stability while giving you opportunities to reach your personal goals. Although your financial priorities may fluctuate during different stages of life, it's never too late to start making positive financial decisions. Start by checking your credit score for free today.

If I could turn back time, here's a list of 7 decisions I would've made differently years ago.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.

There are many ways to avoid financial stress and consistently have spendable wealth. Here are 6 tips to become independently wealthy.